- How financial forecasting and budgeting can help control costs and improve profitability

- The importance of tax strategy in financial planning

- Why management-run companies sell for higher multiples

- How Acquira’s ACE Framework can help you improve financial management

Financial management – whether through effective forecasting and planning or maximizing tax advantages – plays a critical role in the success and sustainability of small businesses.

Effective financial management encompasses several key areas vital for business growth and profitability.

Through financial forecasting, businesses can anticipate future needs and make informed decisions. Budgeting is crucial in tracking income and expenses, setting goals, and optimizing resource allocation.

Implementing tax savings strategies helps minimize tax liabilities and enhance profitability.

Managing debt and credit responsibly ensures healthy finances.

One of the best financial management strategies is maximizing sale value by moving the business from owner-led, where the entrepreneur is the focus of all aspects of the business, to one with a leadership team – increasing the multiple that the business can sell for.

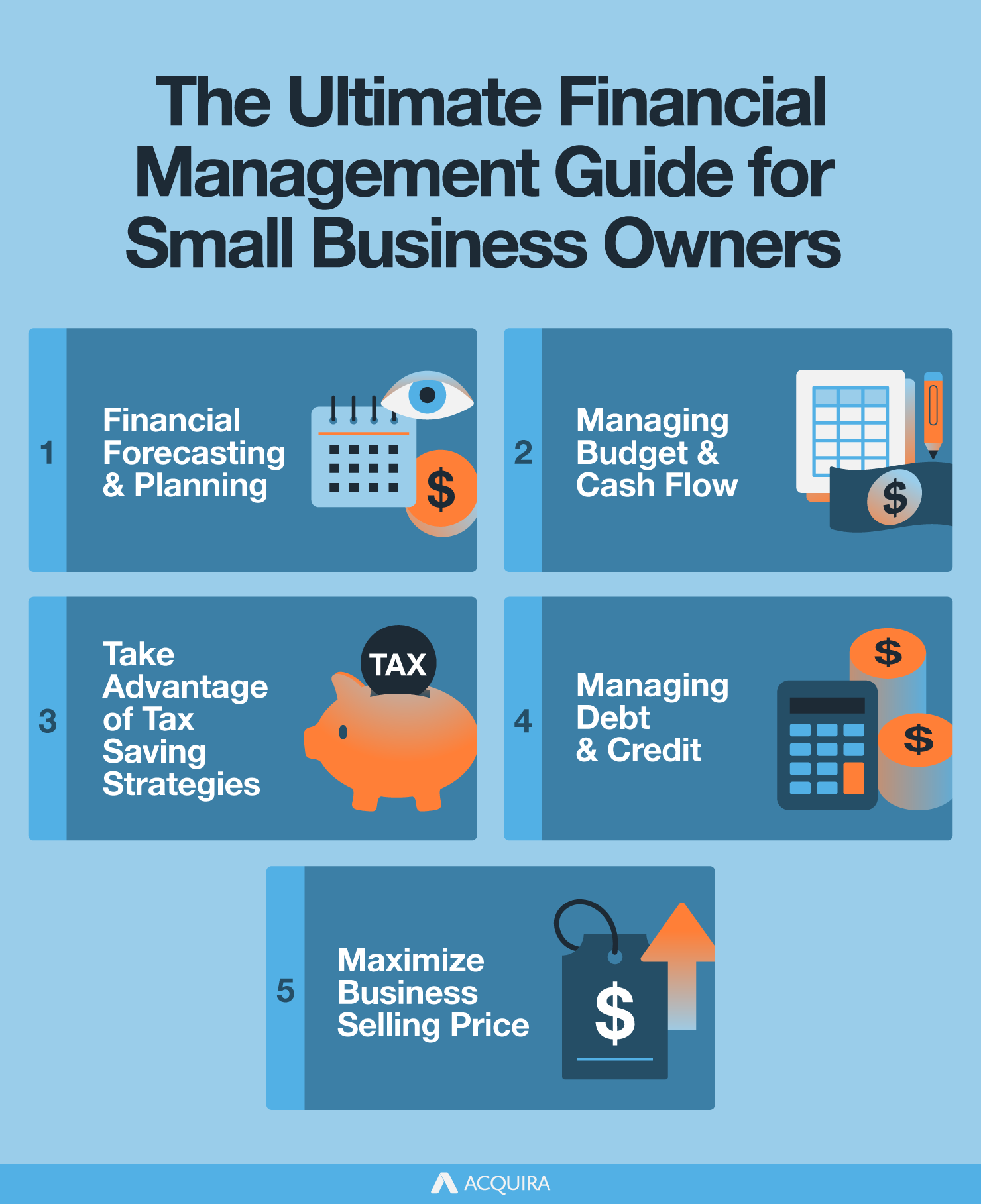

Here is a look at five strategies for financial management.

What is ACE and How Can it Help?

Acquira's ACE Framework is designed to move a small business from an owner-centered operation to a management-run business, giving the owner-operator a chance to step out of the day-to-day operations after the first few months.

This means forming a leadership team where each department has a specific vision and critical performance indicators (KPIs).

This can help improve the new owner's work-life balance and give them time to focus on larger strategic objectives like overall financial management.

An ACE company also has a good grasp of strategic planning and is adept at setting realistic goals for the short-term (1-3 years), mid-term (4-7 years), and long-term (10+ years).

1. Financial Forecasting and Planning

Proper financial forecasting and planning are essential for any small business. It allows for more accurate projecting of revenue and expenses, which must be regularly monitored and adjusted, and creates the basis for setting realistic goals.

Here's a look at financial forecasting and planning for a small business through the lens of a plumbing company.

Forecasting Revenue and Expenses: This involves analyzing historical market trends and performing a cost/benefit analysis on prospective projects to decide which projects to invest in and more accurately forecast future sales, revenue, and expenses.

Based on Acquira's experience in the plumbing industry, each truck performing essential residential services should generate around $200K in revenue with a 50% gross margin. This rises to $300K with a similar gross margin of 50% for slightly more complicated residential work like gas work or repairing water heaters.

Each truck performing more advanced underground work on water mains and gas lines can generate $350-400K with a 60-65% gross margin.

The same should be done with expenses, including materials, equipment, employee wages, and overhead costs.

By forecasting revenue and expenses, a small business owner can make informed decisions about resource allocation and identify potential financial gaps.

Setting Realistic Goals: Based on the financial forecasts, any company can set realistic financial goals for both short- and long-term periods.

One goal might be to increase revenue by a certain percentage each year or reduce expenses in specific areas. Setting goals provides a clear direction and helps the company stay focused on achieving its financial objectives.

Regular Monitoring and Adjustment: Financial forecasting and planning are ongoing processes that involve regular communication with the respective managers of each department.

This means regularly monitoring each department's financial performance against forecasts and making necessary adjustments to the financial forecast.

If actual expenses exceed projections, a company may need to cut costs or find new sources of revenue. Regular monitoring and adjustment enable the company to stay proactive in its financial management and adapt to changing market conditions.

This also involves setting realistic KPIs and routine checkups with team members to ensure goals are met.

2. Managing Budget and Cash Flow

Managing the budget and cash flow is vital for the financial stability of a small business such as an HVAC company.

Create a Detailed Budget: The HVAC company should develop a comprehensive budget that outlines all revenue sources and expense categories, including service fees, equipment sales, and maintenance contracts, as well as expense categories like employee wages, equipment maintenance, and marketing costs.

By estimating income and expenses, the company can set realistic financial goals and allocate funds accordingly. This includes knowing how much to allocate for growth, for example.

A separate budget should be created for each department with the participation of department heads, thereby keeping them accountable going forward.

Monitor and Control Expenses: Another way to manage the budget and cash flow is to monitor expenses to ensure they align with the budget closely. The ACE process includes Mappa company's various processes and then reengineering them where necessary them to reduce costs.

For example, an HVAC company could implement cost-saving measures, such as negotiating better deals with suppliers for equipment and materials, optimizing inventory management to reduce carrying costs, and implementing energy-efficient practices to minimize utility expenses.

By actively managing expenses, the company can control costs and maximize profitability.

Invoice and Payment Management: Efficient invoicing and payment processes play a significant role in cash flow management, especially if the time to collect on accounts receivable can be reduced.

This could include using software to streamline invoicing.

3. Take Advantage of Tax Saving Strategies

Small business owners can use several tax-saving strategies to minimize their tax liability and maximize their after-tax income.

Here are some key strategies to consider:

Entity Selection: Choosing the proper legal structure for the business, such as an S-Corporation, C-Corporation, or LLC, can have significant tax implications.

Each entity type has different tax rules, benefits, and shortcomings, so it's essential to consult with a tax professional to determine the most tax-efficient structure for the business.

Deductible Business Expenses: Small business owners should diligently track and document all business-related expenses to take advantage of tax deductions.

This includes office supplies, travel, marketing and advertising costs, professional fees, and employee wages.

Business owners can reduce their taxable income by identifying and deducting eligible expenses.

Retirement Plans: Contributing to retirement plans such as a Simplified Employee Pension (SEP) IRA, a solo 401(k), or a SIMPLE IRA helps small business owners save for retirement and provides tax benefits.

Contributions to these plans are typically tax-deductible, reducing the business owner's taxable income.

Tax Credits: Small business owners should explore available tax credits, such as the Small Business Health Care Tax Credit, Work Opportunity Tax Credit, or Research and Development Tax Credit.

If you are a small business owner, utilizing the Section 179 expense reduction can be beneficial. This will allow you to deduct the complete cost of qualifying equipment and software purchases in the year they are put into service, rather than spreading out the deduction over multiple years.

Tax credits directly reduce the tax owed, providing a dollar-for-dollar reduction in tax liability.

One of the best ways to take advantage of all applicable tax benefits is to engage a qualified tax professional specializing in small business.

(Tax law can be complicated, so entrepreneurs should speak with a tax professional. None of the above should be interpreted as specific recommendations for any small business owner.)

4. Managing Debt and Credit

Managing debt and credit is crucial for a small business's financial stability and success.

Below is a quick outline of strategies to effectively manage debt and credit.

Develop a Debt Repayment Plan: Create a repayment plan that outlines the schedule and amounts for paying off existing debts.

Prioritize high-interest debts and allocate a portion of the business's income towards monthly repayment.

Maintain Good Credit Practices: Pay bills and obligations on time to establish and maintain a positive credit history.

Timely payments can help improve the business's credit score and make it easier to access credit in the future.

Use Credit Wisely: When utilizing credit, do so strategically and only when necessary. Avoid maxing out credit limits and maintain a reasonable debt-to-income ratio.

Review credit card statements and loan terms regularly to ensure accuracy and identify potential issues.

Remember, managing debt and credit requires discipline, careful planning, and regular monitoring. By adopting these strategies, small businesses can maintain healthy financial habits and position themselves for long-term success.

5. Maximize Business Selling Price

One of the best financial management strategies for small business owners is to maximize how much the business will sell for.

This will get them the most money when they're ready to retire or move on to the next financial endeavor.

Owner-led business: Most owner-led businesses generate $1 million or less in EBITDA (earnings before interest, taxes, depreciation, and amortization).

One person has to wear many hats – from sales to finance to training to project management, to name a few. The owner has little time outside the day-to-day operations to plan for the future and grow the company.

The entire operation revolves around one particular individual, making their replacement a challenging task. This makes the transition to a new owner fairly challenging.

Most businesses like this sell at a multiple of 2-3X.

Management-led: Most businesses that generate $2 million or more in EBITDA are almost certainly management-led.

A leadership team and mid-level managers oversee all aspects of the operation. There are standardized procedures, job descriptions, and electronic systems. It's relatively easy to transition to new ownership.

Businesses like this will usually sell for between 5-6X.

The difference: Selling an owner-led business will yield as much as $3 million for the owner, whereas selling the management-run one could bring in as much as $12 million, a difference of $9 million.

So getting a management team in place can yield significant returns for a small business owner.

Conclusion

Effective financial management is vital for small businesses.

It encompasses financial forecasting, budgeting, tax savings, debt and credit management, and, along with other strategies, maximizes sale value.

Financial management is crucial for small businesses to achieve stability, optimize resources, and position for long-term success.

Acquira's ACE Framework helps businesses transition from owner-led to management-run. Suppose you're interested in buying your own business. In that case, the Accelerator Program will teach you everything you need to know about business acquisition and provide more support through the process than you thought possible. But space is limited. Fill out the form below to see if you're eligible.

Key takeaways

- Financial forecasting helps anticipate needs so you can plan ahead.

- Budgeting tracks income and expenses sets goals, and optimizes resources.

- Tax savings strategies minimize tax liabilities and improve profitability.

- Managing debt and credit ensures a healthy financial position.

- Moving from an owner-led business to a management-run can help maximize sales value.

- Acquira's ACE Framework can help transition from owner-led to management-run

- Management-run companies usually sell for 5-6X EBITDA

Acquira specializes in seamless business succession and acquisition. We guide entrepreneurs in acquiring businesses and investing in their growth and success. Our focus is on creating a lasting, positive impact for owners, employees, and the community through each transition.