- Motivations For Selling A Business

- The Acquisition Process: Steps In Buying An Existing Business

- Finding The Business

- Pre-LOI Diligence

- Pre-LOI Letter

- The Letter of Intent

- Post-LOI Diligence

- SBA Lender

- The Stress Test

- The Business Plan

- QE Analysis

- The Asset Purchase Agreement

- Exchanging Money

- Walking Away

- Conclusion

- Key Takeaways

Many people think that when you own a company, it needs to be built from scratch – pulled by the bootstraps from the ground floor up to the executive suite.

But the reality is that many business owners buy a business or a company after it’s already been operating for some time. Acquiring an established business offers advantages like an existing credit history, stable cash flow, and proven operations, which can reduce risk and provide a solid foundation for growth. This comes with its own pros and cons, but buying an existing company is a great way to step into an ownership position right away.

You may also be looking to expand a business you already own or acquire a company that can complement your offerings in a unique way. It's important to ensure the business you choose aligns with your interests and skill set, as this increases your chances of success and satisfaction. Whatever the reason, our business buying guide should help you on your journey.

Buying an existing business is an attractive alternative to starting from scratch. It also gives you more control over the business's direction, allowing you to leverage established processes, customer relationships, and operational structures from day one.

Initial Insights on Buying a Business

Buying an existing business is an attractive alternative for many aspiring business owners who want to avoid the uncertainty and high startup costs of launching a new business from scratch. With more than 500,000 businesses changing hands each year, the market for buying an existing business is robust and full of opportunity. This process allows you to step into a business that already has operations, customers, and revenue, giving you a head start compared to building a company from the ground up.

However, buying a business is not as simple as signing a check. It involves a series of important steps, including identifying the right business, evaluating its value, reviewing financial statements, securing financing, and negotiating the deal. As a business owner, it’s crucial to understand both the advantages and challenges of buying an existing business. By approaching the process with a clear understanding of the market, the business’s financial health, and your own goals, you can make a smart investment that sets you up for long-term success.

Benefits of Buying a Business

There are many compelling reasons why buyers choose to purchase an existing business rather than start a new business from scratch. One of the biggest benefits is immediate cash flow—since the business is already up and running, you can start generating income from day one. This reduces the risk and uncertainty that often come with launching a new venture.

Buying an existing business also means inheriting a proven business model, an established customer base, and valuable brand recognition in the market. These factors can make it easier for a new owner to maintain profitability and grow the business further. Additionally, you gain access to existing relationships with suppliers, vendors, and employees, which can help ensure a smoother transition and continued success. For buyers looking for a profitable business with a solid reputation, purchasing an established company can be a smart and strategic move.

Motivations For Selling A Business

There are any number of reasons that people may want to sell a business after they’ve created it.

Retirement

Some people are looking to retire. This is becoming increasingly true as more baby boomers approach retirement age. In fact, it’s estimated that over the next two decades, more than 10 trillion dollars worth of small businesses will need to switch hands from baby boomers to someone else.

These people have built their businesses, hired employees, and developed a reputation over many years of hard work. They are looking for a trustworthy steward for their life’s work.

They want to know that their employees will be protected, the reputation they built will last, and the business they created will continue to be successful. The former owner can often provide valuable insights and guidance to the new owner during the transition, helping ensure a smoother handover and a clearer understanding of the business's history and operations.

Burnout

Burnout can come in a number of forms but, generally speaking, it’s people who are tired of what they’re doing. Managing a business can often feel like more than a full time job, leading some owners to seek an exit.

Maybe they no longer like the work, maybe they feel like they’ve done all they can do, or maybe they just don’t find it challenging anymore. Whatever it is, this can be a great scenario for a buyer.

Lack of Success

If the company just isn’t making enough money, the owner may want to sell.

These businesses come with their own problems, but if the buyer truly believes they can turn things around, it may make for an excellent opportunity. It is important for both parties to negotiate a fair price that accurately reflects the business's current challenges and its future potential.

Another Opportunity

Some people own multiple companies. Many businesses are bought and sold as owners shift their focus or pursue new ventures. It’s often the case that they may want to sell one of their businesses in order to concentrate on another company, or maybe they just want to spend more time with friends and family.

Health Problems

This isn’t something that people like to talk about, but sometimes owners will need to bow out of an endeavor because their health is deteriorating. This is certainly unfortunate, but it can create a good opportunity for buyers.

It also allows the founder to step back, recuperate, and possibly enjoy different activities that they weren’t able to do when working full-time.

These founders often want to see their businesses and employees in good hands.

These are just a few examples of why people may want to sell their business. But really, there are myriad possibilities. They all offer a unique opportunity for buyers to step in and make the company their own.

The fact that someone else started the business shouldn’t dissuade you from buying it. It can actually be a great way to grow a company even more and improve the lives of all stakeholders within the business, from upper management down to the new intern.

Once you’ve decided that buying a business might benefit you, it’s time to start. We’re providing this roadmap to help you navigate the process. Of course, at any point, members of Acquira’s community can avail themselves of our resources. In fact, we encourage it.

For more info, please check out our Acceleration Gauntlet.

Types of Businesses to Buy

To understand how to buy a business, you should determine what type of business you should buy. You’ll find a variety of options to suit different goals and budgets. Small businesses are often a popular choice for first-time buyers, as they typically require less capital and can be easier to manage on a day-to-day basis. Franchises offer another path, providing a proven business model and ongoing support from the franchisor, which can be especially helpful for those new to business ownership.

For those seeking a larger opportunity, established companies with a strong customer base and track record can offer stability and significant growth potential, though they may require a larger investment. Business brokers play a key role in this process, helping buyers find suitable businesses, evaluate their strengths and weaknesses, and navigate the purchase from start to finish. Whether you’re interested in a small business, a franchise, or a larger company, working with experienced business brokers can help you make an informed and confident purchase.

Pre-Purchase Considerations

Before you commit to buying a business, it’s essential to take a close look at several key factors. Start by thoroughly reviewing the business’s financial statements to understand its cash flow, profitability, and overall financial health. Analyze industry trends and market conditions to ensure the business is well-positioned for future success. Buyers should also consider their own financial resources and ability to secure a business loan or other forms of debt financing, as these will impact both the purchase and ongoing operations.

Due diligence is a critical part of the process. This means carefully examining important documents such as contracts, leases, and tax returns to identify any potential risks or liabilities. By taking the time to conduct thorough due diligence, buyers can avoid costly surprises and make sure they’re investing in a business with real value and growth potential.

The Acquisition Process: Steps In Buying An Existing Business

Assessing Your Budget & Resources

A realistic assessment of your budget and resources is a crucial step before buying a business. Start by calculating the startup costs required to purchase and operate the business, including any necessary upgrades or working capital. Review your own financial situation—consider your credit score, available savings, and current income—to determine how much you can comfortably invest.

If you need a business loan to finance the purchase, be prepared for lenders to require a personal guarantee, which means you’ll be personally responsible for repaying the loan if the business cannot. Carefully weigh the risks and rewards of taking on debt, and make sure you understand the terms of any financing agreement. By aligning your resources with the needs of the business, you’ll be better positioned to succeed as a new business owner and make the most of your investment.

Defining Your Investment Thesis

Defining your search criteria is an excellent first step to figure out how to buy a business. You need to decide what kind of business you want. That means articulating an investment thesis.

An investment thesis describes the criteria you are looking for in a deal. Some things to consider might include:

- The size of the business (earnings)

- The locations where you are interested in living

- The industries you are interested in

- How much time you can spend working in/on the business

- Other factors that are more (or less) important to you such as recession resilience and maximum valuation

Be clear about what you don’t want. That way you can quickly disqualify any deals that don’t make sense. You avoid wasting your time and ensure you only concentrate on pursuing deals that fit your lifestyle and goals because they match your criteria.

Finding The Business

Finding a business can take some time. But the more effort you put into the process, the better the results will be.

There are two different categories of deal flow: on-market and off-market.

On-Market Deals

On-market deals are simply brokered and publicly listed deals that are listed on websites like BizBuySell or LinkBusiness. This is where most buyers start. Once they find something they like, they reach out to the business broker.

Brokers are experts on how to buy a small business.

It’s good practice to build a rapport with the broker. A positive relationship with these people can help ensure you find deals before they’re made publicly available, resulting in businesses that can be had for a better price and are a better fit for you personally.

Off-Market Deals

Off-market deals are anything the buyer goes out and finds themselves by connecting directly with business owners. This process can be very time-consuming and often more difficult, but it has benefits.

On the surface, these types of deals often appeal to Acquisition Entrepreneurs. Many burgeoning buyers enjoy finding sellers directly and circumnavigating brokers and competition from other buyers.

While cutting out the middle man and the person bidding against you is certainly a tempting idea, it’s important to note that finding off-market deals requires a lot more work.

In order to find off-market deals, you need to cold call business owners or send out cold emails. Assuming you find someone who’s interested, you need to go through an often lengthy process to gather the appropriate financial and legal documents yourself.

Just imagine spending weeks poring over the backs of napkins to discover that the company owes its IT guy back pay from 2016.

A big part of the off-market deal process is setting out realistic expectations with the seller about what their business is really worth.

Although off-market deals can sometimes be found, it is a fact that the most productive deal flow originates from brokers. Brokers know how to do the exacting legwork necessary to close a deal. They get paid to do it, so they don't sacrifice their personal life or other work like a maverick buyer would have to in order to ensure a deal's viability.

These brokers are well-situated in their local communities and usually have deals coming to them. Rather than taking them out of the equation, successful buyers usually build relationships with many brokers to ensure they hear about the best deals first.

Pre-LOI Diligence

Before even considering submitting any kind of proposal, you need to analyze the business. During this phase, you’re getting certain key questions answered about the business's operations and finances.

This helps you ensure that the company actually matches your investment thesis and that there are no obvious red flags or black flags.

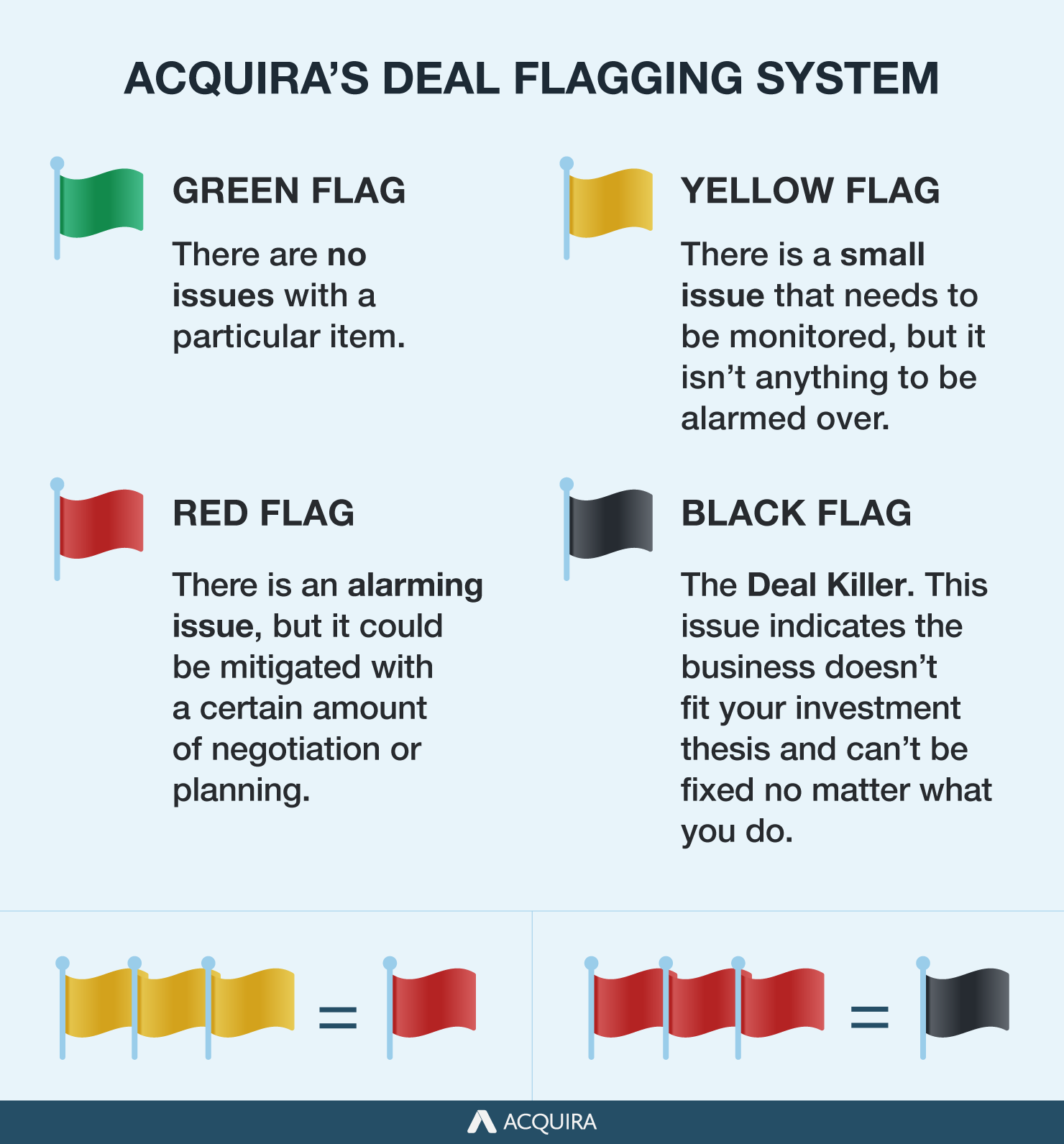

Acquira’s Deal Flagging System

There are issues that you’ll come across when analyzing a business that will cause varying degrees of concern.

We often use the terms Red Flag and Black Flag to indicate how alarmed you should be. More than just cool sounding names for 80s punk bands, these help us determine whether an issue is negotiable or not.

A Red Flag is an issue that is alarming, but could be mitigated with a certain amount of negotiation or planning.

A Black Flag is a deal killer. It’s an issue that indicates the business doesn’t fit your investment thesis and it can’t be fixed no matter what you do.

We also use the term green flag, which means there are no issues with that particular diligence item. And a yellow flag means there is a small issue that we need to keep an eye on, but is nothing to be alarmed about.

Three yellow flags constitute a red flag and three red flags make a black flag.

One example of a red flag might be a business whose earnings have declined over the last three years. A downtrend like that likely doesn’t fit your investment thesis and indicates a business you should avoid. An example of a black flag could be a company that receives most of its income from a single customer.

We’ve compiled a list of Pre-LOI Diligence questions that you can check out here.

During this phase, you should create financial models that forecast the performance of the business in a best, okay, and worst case scenario. Once you have all of this information, you are in a much better position to understand if the work of getting an LOI in place, securing the deposit, and all the other minutiae of beginning the deal process will be worth it.

Acquira offers very detailed training around pre-LOI diligence, including diligence calculators, financial model templates, and more. We also have weekly calls with our team to go over any questions that people have about the process. You can learn about all of these resources in our Acceleration Gauntlet

Pre-LOI Letter

Once you’ve selected a business you like and decided that you want to move forward, you need to make your intentions known.

At this point, the interested buyer can issue what is usually referred to as a Pre-LOI Letter (LOI stands for Letter of Intent). A pre-LOI letter allows you to figure out the high level terms of a deal with a seller before you spend a more considerable amount of time and legal costs creating a full LOI. Since a pre-LOI letter is simple to put together, it will also allow you to show serious purchasing intent sooner rather than later, which will engage the seller and keep other buyers at bay.

These pre-LOI terms can include the purchase price, the deal structure, how the seller will transition out of the business, how long the post-LOI diligence period will be, and more. The seller may also consider the buyer's background, experience, and financial position when evaluating the seriousness of the offer.

As you start to get some of those high-level items outlined, you should also include your SBA lender in the process so they can give you reasonable certainty that they can fund the deal based on the terms the two parties have started to discuss.

The Letter of Intent

Next up, you issue a full letter of intent.

LOIs are usually non-legally binding documents that are an integral tool in the process of buying a small business, as online marketing influencer Jeff Bulas explains in his blog:

“In complex negotiations, such as the purchase or sale of a business, multiple contracts between buyers and sellers usually occur. This process may take a substantial amount of time and lead to misinterpretation later on. Oral agreements also have contractual force. A letter of intent written before the final closing and drafting of actual language can fix the main issues under discussion in written form and clearly lay down rules, such as confidentiality of information. Writing the LOI serves to focus on issues and identify neglected matters. It may also assure an insecure seller that the buyer is serious and vice versa.”

In the LOI, you will work with a legal team to refine the language of your initial agreement. You can either work with your preferred legal team or with Acquira’s preferred legal team.

Be prepared to wait during this period. While the LOI process can take as little as a week, sometimes it can take as much as a month. The length will depend on the broker, the seller, and the seller’s attorneys.

Be prepared to wait during this period. While the LOI process can take as little as a week, sometimes it can take as much as a month. The length will depend on the broker, the seller, and the seller’s attorneys.

The lawyers will review the information and ensure that each stipulation in the agreement is spelled out in contractual language.

Once both parties agree to it and sign it, that’s when you’re under LOI.

Refundable and Non-Refundable Deposits

Since the market heated up last year, many sellers will request a good faith deposit. These deposits are meant to ensure that you’re sincere in your interest in acquiring the company. Sometimes these are refundable and sometimes not.

Non-Refundable Deposits, a Mini-Case Study

In one instance, Acquira was under LOI with a roofing company.

In order for Acquira to actually get under LOI with the company, they had a hardline stance that required a deposit. The deposit was non-refundable.

We were able to negotiate the deposit price lower, but whether the deal was signed or not, we weren’t going to get that money back. This may seem ridiculous from the outside, but if it’s a deal you really like, you can be open to the possibility. Otherwise, you should ignore non-refundable deposits.

Deposits obviously represent a certain amount of risk, but they do make sense from the seller’s point of view. Indeed, deposits have become a standard operating procedure for many entrepreneurs.

If potential buyers constantly send them LOIs, they receive a lot of classified company information. These potential buyers gain access to their social security information, their tax returns, their competitor information, and basically all of their financial information.

As a matter of course, many companies have started asking for a deposit to compensate for the work involved in providing this information. This helps cover the costs accrued during this process.

Post-LOI Diligence

Once an LOI is signed, the buyer will enter into a few processes that happen in tandem: the post-LOI diligence process and the process of working with your SBA lender.

This deeper due diligence process will vary depending on the nature of the transaction and the interpersonal dynamics. High value acquisitions will undoubtedly require a high level of financial, operational, and legal due diligence.

The purpose of the post-LOI diligence period is for the buyer to 100% confirm all of the information that was collected and analyzed during the Pre-LOI Diligence period.

The buyer is acquiring the company “warts and all,” they need to know as much information about the company as possible before closing the deal. If a company has a substantial tax liability or a sizable claim against it, you’ll want to know that as soon as possible.

Given that the buyer is acquiring the company “warts and all,” they need to know as much information about the company as possible before closing the deal. If a company has a substantial tax liability or a sizable claim against it, you’ll want to know that as soon as possible.

It may not send you running for the hills, but it’s important information to have regardless.

Acquira can provide documents with a few hundred questions to help make this process easier. The categories include financial operations, employee information, general information, IT, marketing, sales, and more. We can also connect you with our preferred vendors to help with the due diligence process.

Each category requests the specific materials needed to assess the business properly. These requests are sent as soon as possible after the LOI is signed. That allows the broker to start gathering information while you worry about the other parts of the process happening at the same time…

SBA Lender

While conducting the due diligence process, you should also work with an SBA lender. As we mentioned, you should already be in touch with at least one lender (though usually, we recommend shopping multiple lenders).

The lender should already be familiar with the business and the high-level terms of the deal by this point.

The SBA is a United States federal agency that helps small businesses get loans. The SBA doesn’t issue loans itself but works with lenders and other lenders to help them overcome obstacles to lending. This can include guaranteeing loans, reducing risk, and helping to source capital. At its core, the SBA funds, licenses, and regulates investment funds that can then lend to small businesses.

Eligibility requirements for an SBA loan include:

- The business must be for-profit.

- The business must be U.S. based.

- You must have invested in the business yourself.

- It’s best to have a good credit score of 700 or more.

Ideally, the SBA lender is one you already have a relationship with. It could be someone you’ve been lending with for 20 years or 10 months, as long as they have an SBA program, which most lenders do. If you are part of Acquira’s programs, we will introduce you to our preferred lenders.

It’s important to note that lenders will rely heavily on the cash flow and assets of the business you are targeting to service the debt. However, they will also take a deep dive into your financial profile and ideally, they like to see that you have personal assets (real estate for example) that can serve as collateral for the loan.

Other Funding Options

Not everyone will qualify for SBA financing and some people might prefer more creative and flexible financing options. But there are other options.

One is to work with a private lender and/or investor. Opting for private financing may incur slightly higher financing costs, but it enables you to structure your purchase in a manner that maintains cash flow. Utilizing this can expand your business. Deferred interest and dividends are both things you could consider in this scenario.

Private financing options can also make more flexible debt agreements which can foster additional financing opportunities in the future. This may also increase the possibility of higher payouts for both the primary owner and financing partner when you choose to exit the business in the future.

The Stress Test

When buying a business, you should always perform a stress test. The test allows you to see roughly how long the company can stay in business if you don’t receive any new customers or clients.

The test is a worst-case assessment. Generally speaking, things would never get as bad as they are imagined to be in the stress test. But it’s useful to know how much damage a business can take before it becomes unsalvageable.

When buying a business, the process is carried out with the lender. After all, they want to make sure the business is a solid investment as well. The nice thing about this stage is that it can actually give you a better understanding of the business itself. The lender may ask certain questions that you didn’t think to ask.

Don’t be afraid to ask questions at any stage. The lender is there to help ensure your success. For example, they will want a pro forma financial model, financial reports for your business based on hypothetical scenarios. Essentially, this is a stress test. It’s a three year projection that will look at how the business will perform in the market with your marketing plan, for example.

Rest assured, the lender will see you as a secure option for the loan. It also serves to give the buyer a better understanding of what different variables can impact the business that you can control.

When performing a stress test, you can apply certain scenarios that may negatively impact your business. So, if there’s negative growth or the business fails for whatever reason, how much could you lose? Maybe you’ll discover the business can survive three years of negative growth before stabilizing in year four. They want to see if, during those three years of negative growth, the lender can still service its debt.

lenders will be able to answer most of these questions themselves, with their own underwriting team. But the lenders want to see the buyer figuring out as much of this information on their own as possible. It demonstrates that the buyer has an understanding of the business and the economy.

The Business Plan

The lender will also request a business plan. This is part of the SBA loan process but ideally, you would have developed a business plan before sending the LOI. By this point in the deal, the plan should be very in-depth.

It is crucial to incorporate the business history and the rationale behind your investment interest.You’ll also include its current marketing plan, its current strengths in terms of niche pricing, and a SWOT analysis.

The SWOT analysis looks at a business’ Strengths, Weaknesses, Opportunities, and Threats. This includes an analysis of your competition.

You will also need to develop a current organization chart and include any changes you plan on making to that chart. So, whether you plan on hiring a General Manager, a bookkeeper, or any other new employees that grow the organization.

Many of these are due diligence questions and you will already have 80-to-90 percent of the information. It will simply be a matter of putting it all together. The lender just wants to see that the buyer did their homework.

Below, you’ll find a list of some of the most important information you will need to provide about your personal finances and plans for the business when applying for an SBA loan.

- Business plan

- Marketing plan

- Growth plan

- Pro forma financial model

- Personal tax returns

- Personal Income

- Business tax returns

- List of assets

QE Analysis

As we mentioned, the SBA process is happening at the same time as the due diligence process. The most important part of this deeper diligence process is the quality of earnings analysis. This analysis confirms the financial statements of your target business and ensures you aren’t making critical errors based on the financial statements you received from the seller.

Acquira can connect you with our preferred diligence vendors once you are part of our programs, including vendors for the QE analysis.

There’s no such thing as a stupid question at any point in this process. It’s better to ask a potentially silly question than to acquire a faulty business.

If there’s an aspect of the deal that doesn’t make sense to you, make sure to ask someone. Ask the seller or the broker or the lender. They will give you clarification. If you are part of Acquira’s buyer community, you will have access to our team and we can provide structured guidance.

Just make sure you take your time and never feel pressured. A small business purchase is an investment and should never be viewed as a gamble.

The Asset Purchase Agreement

Once you’ve completed your due diligence, the lender will still want to see a few more things.

First, they will want the buyer to have a life insurance policy for the amount of the loan. They will also require a third-party appraisal of the deal.

After the SBA gives the green light, the underwriters have reviewed it, and the sellers agree to move forward, you enter an asset purchase agreement, or APA.

This is when the seller’s legal team gets involved. Depending on the lawyer, this step can take anywhere from a week to a month to complete.

The seller’s lawyers will pore over all of the documents and discuss the finer points of the contract. If an LOI is two or three pages, the APA is often 20 pages. This is the final document that definitively outlines every aspect of the transaction.

You’ll also discuss the future involvement of the sellers at this point. This will specify whether you will continue using their licenses, whether they will stay on for a period to help with the transition, whether they will help train new management, and whether the seller will continue to provide certain services during the transition period, along with other similar items.

Exchanging Money

Once the APA is agreed upon and signed, the lender will put you in touch with a Title Escrow Company.

The lender will fund their escrow account, and, at that point, you can finally sit down and sign the closing documents. During this stage, maintaining trust and continuity is important for retaining many customers, as a smooth ownership transition helps preserve customer relationships and loyalty. Once everyone signs, the funds are released to the seller and you are officially the owner of the company.

Numbers

Math can be daunting to some people and there is a lot of math that will come up when looking at the financial statements of a business. Don’t let this sway you as it’s important to understand when buying a business. We recommend reading the book Financial Intelligence from the Harvard Business Press to help you understand the language.

Most people who are afraid of math are actually afraid of numbers. But these numbers shouldn’t scare you. For the most part, any math you bump against in closing a deal will be little more than simple addition and subtraction, with a little division and a few percentages thrown in for good measure.

You can do nearly any math you encounter on your cell phone.

Not being scared of numbers will actually serve you well. These numbers will tell a story. The past three years' management of the business, employee satisfaction, and potential issues are all revealed through these.

In addition to basic math, buyers should be aware of basic finance and accounting concepts. These are needed not only to analyze the business but also to run it effectively.

At the most basic level, every buyer should:

- Understand the difference between a Balance Sheet and a Profit & Loss (P&L) Statement

Balance sheets report a company’s assets, liabilities, and shareholder equity for a specific point in time. Balance sheets give investors and creditors an idea of how well a company manages its resources. A P&L Statement is a summary of revenues, costs, and expenses incurred over a period of time. Also known as an Earnings Statement. A P&L Statement shows whether a company can generate profit through increasing revenue, reducing costs, or both

Walking Away

Acquiring a company requires a huge time investment. It takes months of talking to the seller, talking to the lender, building a rapport, and dealing with the broker.

After two or three months, you may feel like you just want to get the deal done. But at this point, you should take a step back and really look at the deal closely.

It’s easy at this point to let something slide just to close the deal. It becomes hard to remain objective and see the red flags. Ask yourself if the deal is really worth it.

Acquiring a company should never be a gamble. It’s an investment. If, after all of your due diligence and investigation, it feels like you’re gambling, it’s definitely time to reassess why you want to acquire this business.

Never approach a deal thinking “Well, if I’m going to lose, then I lose. But if I win, then I’ll win big.” These deals aren’t just about you. These companies can have 10 or 20 employees who have to feed their families. If you don’t think you’re the best steward of those 20 employees, then you shouldn’t be acquiring it.

At any point in the process, you should feel empowered to walk away from the deal. Don’t make it about pride or ego. Make sure it’s for the right reason.

Ensuring a fresh perspective and a clear mind is integral to Systematic Excellence, a core value that Acquira tries to imbue in all of its acquisition entrepreneurs. Sometimes, after walking away from several deals, buyers have finally found the right business that truly aligns with their goals.

Conclusion

Acquiring a company is a journey – learning how to buy a business is the first step in that journey. It isn’t just about finding something shiny and deciding to buy it. This is going to be a process.

Don’t rush just because you want to get something done. Ensure you follow the proper steps and avail yourself of Acquira’s resources. We have been in the acquisition space since 2015 gathering experience and knowledge so you never feel pressured or overwhelmed. We’re here to help the process run smoothly.

It’s often true that deals don’t close the first time around. But we’ll keep working with you until you find something that inspires you and meets your investment thesis.

If you’d like to learn more about acquiring a company, many of the resources we discussed above can be obtained by signing up for our Acceleration Program. Set up a call with us through the form below and we'll be in touch.

Have you had any bumps along the road of your own acquisition journey? Please share them with us in the comments below.

Speaking of sharing, if you found this article useful, we’d love it if you could share it with anyone who you think could help.

Key Takeaways

- There are many reasons someone may want to sell their business.

- Work closely with the legal team to define the terms of the deal.

- Use well-vetted and reliable vendors at all stages of the process.

- Remember to take a step back and look at the deal with a fresh perspective.

- Don’t be afraid to walk away.

Acquira specializes in seamless business succession and acquisition. We guide entrepreneurs in acquiring businesses and investing in their growth and success. Our focus is on creating a lasting, positive impact for owners, employees, and the community through each transition.